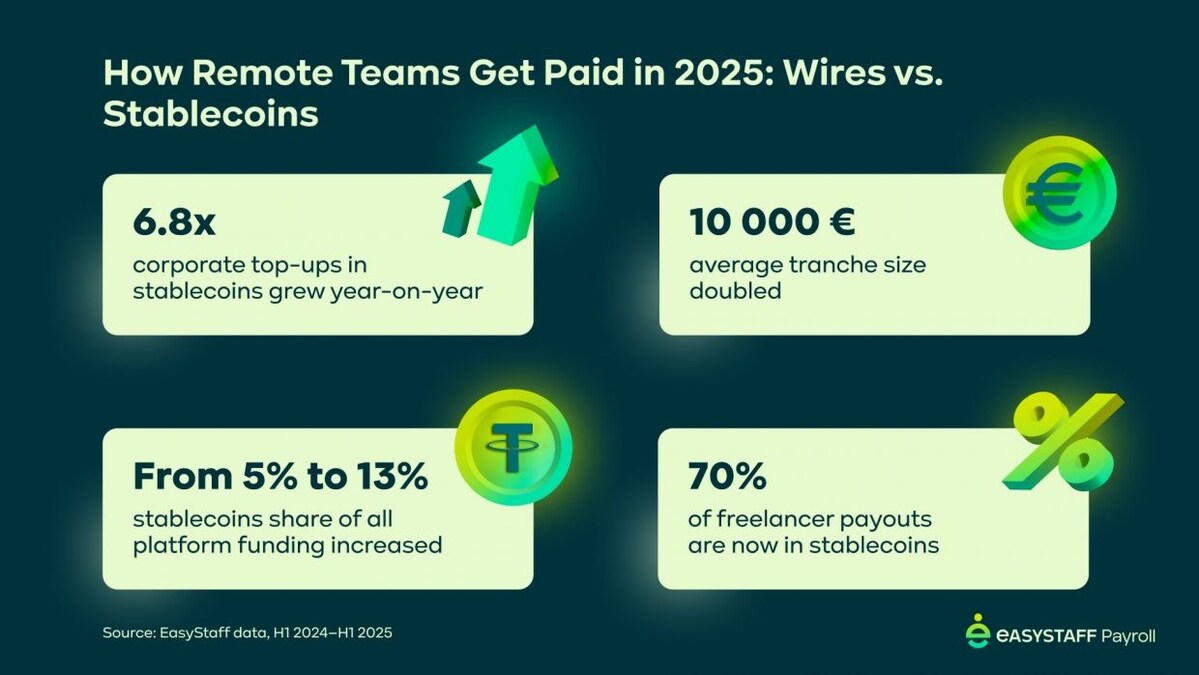

The stablecoin payroll constraint in 2026

Stablecoin payroll in 2026 is defined by a specific constraint: the gap between settlement speed and regulatory compliance. While the technology allows for instant cross-border transfers, the legal infrastructure required to label these payments as "payroll" rather than "property distributions" remains fragmented. This distinction dictates which platforms can operate legally and where the risk lies for employers.

The primary challenge is not the blockchain itself, but the jurisdictional mismatch. A platform might support USDC transfers to a contractor in Brazil, but if the platform lacks a Money Services Business (MSB) license in that state or country, the employer bears the compliance burden. 2026 sees a shift from experimental crypto payroll to regulated fintech solutions that wrap blockchain rails in traditional compliance frameworks like KYC/AML and tax reporting.

This constraint forces a trade-off between speed and safety. Unregulated wallets offer immediate settlement but expose the company to tax audits and labor law violations. Regulated platforms, such as those highlighted in recent industry comparisons, slow the process slightly by integrating verification steps but provide the audit trails necessary for legal payroll. Employers must choose infrastructure that supports both the transaction and the paperwork.

The trend in stablecoins for 2026 is not about replacing fiat entirely, but about using stablecoins for the settlement layer while fiat remains the accounting layer. This hybrid approach addresses the prediction that crypto will be integrated into traditional finance rather than replacing it. For global talent strategies, this means paying in stablecoins can be compliant, provided the payroll vendor handles the regulatory heavy lifting.

Stablecoin payroll 2026 choices that change the plan

Adopting stablecoin payroll in 2026 offers speed and lower fees, but it introduces specific regulatory and operational risks. The decision requires weighing the efficiency of on-chain transactions against the complexity of tax compliance and custody. Most platforms now support major stablecoins like USDC and USDT, but coverage varies significantly by jurisdiction.

Compliance and Tax Complexity

Stablecoin payments are often treated as property, not currency, by tax authorities like the IRS. This means every payroll transaction can trigger a taxable event if the value changes between approval and payout. Employers must track cost basis and capital gains for each payment, adding significant administrative overhead. Platforms like Deel and Eco are integrating tax reporting tools, but the burden of accurate record-keeping remains on the employer. Failure to comply can result in penalties, especially in the EU and UK where new MiCA regulations are taking effect.

Custody and Counterparty Risk

Who holds the stablecoins during the payroll process? Centralized exchanges offer ease of use but introduce counterparty risk. If the platform freezes assets or goes insolvent, payroll stops. Decentralized solutions offer more control but require technical expertise to manage private keys. Many 2026 platforms use hybrid models, where funds are held in regulated custodial wallets until the moment of disbursement. This reduces risk but adds a layer of verification. Employers should prioritize platforms with clear insurance policies and audited custody solutions.

Coverage and Exchange Rate Volatility

While stablecoins are designed to maintain a $1 peg, minor de-pegging events can occur. More importantly, not all stablecoins are accepted everywhere. USDC is widely supported in the US and EU, while USDT dominates in emerging markets. Exchange rates between stablecoins and local fiat can fluctuate during the payout window. Platforms that auto-convert to fiat before depositing into local bank accounts eliminate this risk but add fees. Direct crypto payouts are cheaper but expose employees to volatility unless they immediately convert.

Platform Integration and Automation

The best stablecoin payroll platforms integrate directly with existing HR and accounting software. This automation reduces manual errors and ensures that payroll data flows seamlessly into tax filings. Look for platforms that support smart contract-based payroll, where payments are triggered automatically upon approval. This reduces the time from payroll processing to employee receipt from days to minutes. However, integration complexity can be high for companies with legacy systems.

| Factor | Stability | Cost | Compliance | Speed |

|---|---|---|---|---|

| Traditional Bank Transfer | High | High | Standard | 1-5 days |

| Stablecoin (USDC/USDT) | Medium | Low | Complex | Minutes |

| Crypto Payroll Platform | High | Medium | Assisted | Same-day |

| Decentralized Protocol | Low | Very Low | Self-managed | Instant |

How to choose the right stablecoin payroll system

Automated stablecoin payroll shifts from experimental to operational in 2026. The difference between a smooth rollout and a compliance nightmare comes down to three specific factors: regulatory clarity, custody security, and global coverage. Use this framework to evaluate your options.

Prioritize platforms that explicitly support your jurisdiction’s reporting requirements. In 2026, stablecoin payroll is not just about sending USDC; it is about generating the necessary tax forms and audit trails for each contractor. Avoid solutions that treat crypto payroll as an afterthought rather than a core compliance feature. Check if the provider offers automated withholding for countries with complex tax treaties.

Determine who holds the keys. Enterprise-grade payroll requires institutional custody or multi-signature wallets to prevent unauthorized access. Retail-grade solutions may be cheaper but lack the insurance and governance structures needed for regular payroll runs. Ensure the platform integrates with your existing treasury management tools to maintain a clear separation between operational funds and payroll liabilities.

Global talent means global infrastructure. Your chosen platform must support multiple stablecoins (USDC, USDT, EURC) across different blockchains to minimize gas fees and maximize accessibility for your contractors. Verify that the platform can convert stablecoins to local fiat for contractors who do not want to hold crypto. A lack of conversion options limits your hiring pool to only those comfortable with digital assets.

Payroll should not be a siloed process. Look for platforms that offer API access and integrate with your current HRIS or accounting software. Manual data entry increases the risk of errors and delays. Seamless integration ensures that contractor onboarding, timesheet approvals, and payment execution happen in a single workflow, reducing administrative overhead and improving accuracy.

Understand the total cost of ownership. Some platforms charge per transaction, while others offer flat monthly fees. Consider the hidden costs of network gas fees, conversion spreads, and withdrawal fees. Transparent pricing helps you predict payroll expenses accurately. Avoid platforms with opaque fee structures that can erode your budget, especially when scaling to a larger workforce.

Spotting Weak Stablecoin Payroll Options

Not every platform marketing itself as a 2026 stablecoin payroll solution actually delivers on compliance or speed. Many vendors use "stablecoin" as a buzzword to mask legacy fiat infrastructure, leaving you with the volatility risks of crypto without the settlement benefits. You need to verify whether the platform handles the actual on-chain transfer or if it merely converts your USD to crypto internally and then back to fiat for the worker.

Watch for vague custody descriptions. If a provider does not explicitly state whether they use self-custody, multi-signature wallets, or regulated third-party custodians, treat it as a red flag. In 2026, regulatory scrutiny on payroll providers is intensifying, and opaque custody models can trigger tax reporting errors or frozen funds during audits. Always demand a clear breakdown of who holds the private keys and how insurance coverage applies.

Another common trap is the lack of real-time tax jurisdiction mapping. A platform that simply sends USDC to a global contractor without automatically calculating and withholding local income taxes is not a payroll solution—it is a risky money transfer tool. Ensure the software integrates directly with local tax authorities or provides explicit, jurisdiction-specific withholding rules before you onboard any international talent.

No comments yet. Be the first to share your thoughts!