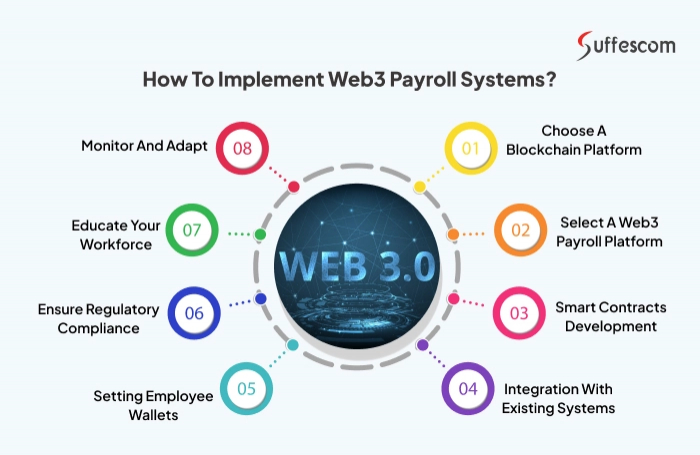

IRS Treats Crypto Payroll as Taxable Wages

The regulatory foundation for crypto payroll rests on a single, non-negotiable IRS classification: virtual currency is property, not currency. IRS Notice 2014-21 establishes that general tax principles applicable to property transactions apply to digital asset payments. This distinction transforms every payroll event from a simple wage disbursement into a taxable disposition of assets.

For the employer, the implications are immediate. When you transfer Bitcoin or Ethereum to an employee, the IRS views this as the sale or exchange of property. If the asset has appreciated in value since acquisition, the company may recognize a capital gain on that transfer, creating a tax liability before the employee even receives their paycheck. Conversely, if the asset has depreciated, the company faces a capital loss. This volatility introduces unpredictable tax outcomes that traditional fiat payroll systems do not generate.

For the employee, the receipt of crypto is treated as ordinary income. The value of the cryptocurrency at the exact time of receipt constitutes taxable wages. This value is subject to standard payroll taxes, including Social Security, Medicare, and federal income tax withholding. The employee’s cost basis is locked in at that moment. Any subsequent appreciation in the asset’s value is treated as a separate capital gain event, taxable only when the employee sells or exchanges the crypto.

This dual-layer taxation creates a complex compliance landscape. Employers must accurately report the wage amount on Form W-2, just as they would with USD. Failure to properly calculate and withhold taxes on the fiat-equivalent value of the crypto at the time of payment can result in significant penalties for both the employer and the employee. The IRS does not distinguish between a paycheck in dollars and a paycheck in Bitcoin; both are wages subject to the same strict reporting requirements.

Stablecoins reduce volatility risk for payroll

In 2026, payroll strategies are shifting away from volatile assets like Bitcoin (BTC) and Ethereum (ETH) toward stablecoins such as USDC and USDT. This transition prioritizes compliance accuracy and minimizes the accounting complexity inherent in paying employees with fluctuating assets.

IRS guidance treats cryptocurrency payments as property, meaning every payout triggers a taxable event based on the value at the time of transfer. With volatile assets, the value of an employee’s paycheck can swing significantly between the moment a company approves payroll and the moment the employee receives it. This volatility creates two distinct risks: accounting mismatches and employee dissatisfaction. A 10% drop in BTC value overnight effectively reduces an employee’s take-home pay without any change in labor effort.

Stablecoins solve this by pegging value to fiat currencies, typically the US dollar. For employers, this eliminates the need to hedge against price swings before every payroll run. For employees, it ensures that the labor they performed is compensated at the exact value agreed upon in their contract, regardless of broader crypto market conditions.

The stability of USDC makes it a primary candidate for payroll integration. Its price action over the last 12 months demonstrates a tight peg to the dollar, contrasting sharply with the wide swings seen in major cryptocurrencies. This stability is not just a convenience; it is a compliance necessity for maintaining accurate books and records.

While stablecoins reduce volatility, they do not eliminate regulatory obligations. Companies must still withhold income taxes and report payments on Form 1099-NEC or W-2, depending on worker classification. The key difference is that the valuation step becomes predictable. Instead of wrestling with real-time oracle data for every transaction, payroll software can rely on the stablecoin’s peg to calculate exact tax liabilities.

This shift is already visible in global compensation trends. Reports from 2026 indicate that stablecoins are becoming the standard for cross-border payroll, particularly in regions with high inflation or unstable local currencies. By decoupling payroll from speculative assets, companies can offer global talent competitive, predictable compensation without exposing their balance sheets to crypto market risks.

Top crypto payroll platforms compared

Selecting a crypto payroll vendor requires matching technical infrastructure to IRS reporting obligations. The four leading providers—Eco, Bitwage, Rise, and Deel—differ significantly in how they handle tax automation, asset custody, and supported chains. These differences determine whether a platform can process compliant W-2 filings or if it merely facilitates volatile transfers without regulatory safeguards.

Eco operates as a dedicated crypto payroll infrastructure provider, emphasizing multi-chain support and automated tax reporting. Bitwage specializes in converting crypto earnings into fiat for local tax compliance, acting as a bridge between digital assets and traditional banking. Rise focuses on global accessibility, allowing employers to pay contractors in stablecoins while the platform handles the conversion. Deel, a broader global payroll giant, integrates crypto payments as one option among many, prioritizing its established legal entity framework over native crypto features.

The following comparison outlines the core compliance and technical distinctions for 2026.

| Platform | Tax Filing Automation | Custody Model | Supported Stablecoins | Country Coverage |

|---|---|---|---|---|

| Eco | Automated 1099/W-2 | Non-custodial (self-custody) | USDC, USDT, DAI | Global |

| Bitwage | Fiat conversion + IRS reporting | Third-party custodian | BTC, ETH, USDC | 180+ countries |

| Rise | Automated tax docs | Custodial wallet | USDC, USDT | 150+ countries |

| Deel | Integrated with payroll system | Custodial partner | USDC, DAI | 100+ countries |

Custody models directly impact liability. Eco’s non-custodial approach means the employer retains control of private keys, reducing counterparty risk but shifting security responsibility to the company. Bitwage and Rise use custodial models, where the platform holds assets, which simplifies operations but introduces third-party risk. Deel’s integration relies on its existing custodial partnerships, blending crypto with its traditional payroll infrastructure.

Tax filing automation is the critical differentiator for IRS compliance. Platforms like Eco and Rise generate automated tax documents, reducing the administrative burden of tracking crypto transactions for tax purposes. Bitwage converts crypto to fiat before payment, simplifying IRS reporting by treating payments as traditional currency. Deel’s crypto features are secondary to its core payroll engine, which may require additional configuration for crypto-specific reporting.

Automated tax reporting simplifies compliance

Crypto payroll introduces a complex taxable event: the moment an employee or contractor receives digital assets, the transaction is treated as ordinary income. Without automated reporting, tracking these events across multiple blockchains and stablecoins creates significant manual bookkeeping errors. Modern platforms mitigate this risk by integrating real-time tax engines that calculate liabilities at the point of transfer.

1. Auto-conversion to fiat for payroll

Many compliant platforms offer automatic off-ramping, converting crypto payments into USD (or local fiat) before depositing into employee bank accounts. This approach removes the need for individual employees to manage tax withholdings on volatile assets. The platform handles the conversion, ensuring that the gross pay matches the fiat equivalent required for tax reporting.

2. Automated 1099 and W-2 generation

For US-based payroll, platforms must generate IRS-compliant forms. Automated systems aggregate transaction data throughout the year to produce accurate Form 1099-NEC for contractors or W-2s for employees. This eliminates the manual data entry that often leads to mismatched social security numbers or incorrect income reporting, which can trigger IRS audits.

3. Immutable audit trails

Compliance requires an unalterable record of every transaction. Reputable platforms maintain an immutable audit trail on-chain and off-chain, linking each payment to its corresponding tax event. This transparency allows accounting firms to verify income and deductions quickly, reducing the time and cost associated with year-end audits.

Ensure your provider generates IRS-compliant tax forms (1099/W-2) and maintains an immutable audit trail for all transactions.

Confirm the platform supports the specific stablecoins you use (e.g., USDC, USDT) and has clear policies on their tax treatment.

Understand whether the platform uses a non-custodial model (where you retain control) or a custodial model, as this impacts liability and compliance obligations.

| Feature | Auto-Convert to Fiat | 1099/W-2 Gen | Immutable Audit Trail |

|---|---|---|---|

| Platform A | Yes | Yes | Yes |

| Platform B | No | Manual | Yes |

Choosing the right crypto payroll solution

Selecting a platform requires aligning technical custody with regulatory obligations. The primary risk lies in how assets are held and reported. You must verify that the provider supports the specific tokens you intend to use and that their reporting aligns with IRS Form 1099-NEC requirements for independent contractors.

Geographic reach determines tax withholding capabilities. If your team is distributed, the platform must handle multi-jurisdictional compliance automatically. Relying on manual calculations for state or local taxes introduces significant liability. Prioritize providers with established partnerships in your key operating regions.

Integration with your existing HRIS is non-negotiable for accuracy. Seamless data flow prevents manual entry errors that can lead to incorrect tax filings. Ensure the platform offers API access or native connectors to your current payroll software. This integration ensures that crypto payments are recorded correctly alongside traditional compensation.

Frequently asked questions about crypto payroll

Is crypto payroll taxable? Yes. The IRS treats cryptocurrency as property. The value of tokens at the time of payment is treated as gross income for both employer and employee, subject to standard withholding requirements.

How do I report crypto wages? Employers must convert the cryptocurrency payment to its U.S. dollar value at the time of payment. This value is reported on Form 941 and included in the employee's W-2 wages.

Can employees refuse crypto pay? Employees can refuse crypto compensation if it violates their employment contract or local labor laws. However, most compliant platforms require explicit employee consent before initiating payments in cryptocurrency.

No comments yet. Be the first to share your thoughts!