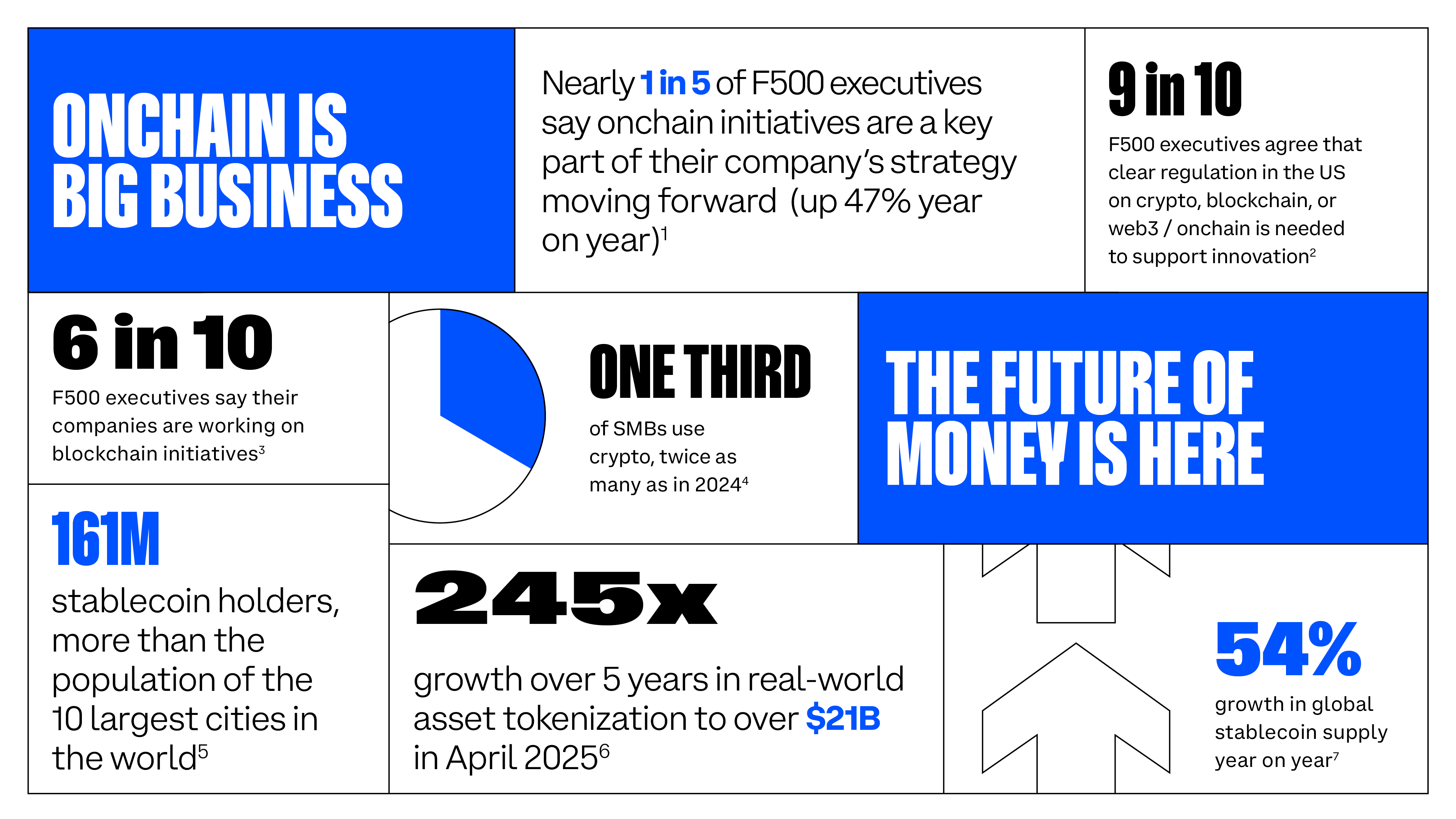

The pivot to stablecoin payroll

The landscape of digital compensation is undergoing a structural correction. In 2026, the primary use case for crypto payroll is shifting decisively from volatile assets like Bitcoin and Ethereum toward stablecoins. This transition is no longer driven by speculative interest but by the necessity of predictable compensation structures and regulatory alignment. Corporate risk management now dictates that employee wages must retain their nominal value from issuance to deposit.

The catalyst for this shift is twofold: emerging regulatory frameworks and the practical demands of global payroll. The European Union’s Markets in Crypto-Assets (MiCA) regulation and the proposed U.S. GENIUS Act establish clear definitions for stablecoins, distinguishing them from securities or unbacked tokens. These laws require issuers to maintain 1:1 reserves in high-quality liquid assets, providing the legal certainty that multinational corporations require for statutory wage obligations.

Using volatile cryptocurrencies for payroll introduces unacceptable accounting complexity and employee risk. A salary paid in Bitcoin may lose 20% of its value between the time it is approved and the time it is received, creating disputes over fair compensation. Stablecoins, pegged to fiat currencies like the U.S. dollar, eliminate this variance. They offer the speed and borderless nature of blockchain settlement while preserving the unit-of-account function essential for payroll.

This stability allows employers to treat crypto payroll as a direct rail for fiat-equivalent value. The technology handles the transfer, but the value proposition is rooted in the predictability of the asset. As compliance infrastructure matures, stablecoins are becoming the standard for cross-border payments, replacing traditional correspondent banking for speed and lower transaction costs without exposing employees to market volatility.

Global payouts require strict adherence to local tax and labor laws

Paying workers in digital assets is not a jurisdictional loophole. In 2026, employers face a complex matrix of regulations that vary significantly by country. The core challenge lies in reconciling the borderless nature of blockchain with the territorial enforcement of labor and tax codes. Misunderstanding these distinctions exposes the company to severe penalties, back taxes, and potential criminal liability.

Tax reporting obligations

Most major economies treat cryptocurrency as property or taxable income, not legal tender. When an employer pays a contractor in USDC or BTC, that transaction is a taxable event for the recipient and a deductible expense for the payer. However, the reporting mechanisms differ. In the United States, payments to foreign contractors still require IRS Form 1099-NEC if the work is performed domestically, or Form W-8BEN for foreign entities. Failure to report these payouts can trigger audits. Employers must ensure their payroll software generates accurate transaction records that satisfy local tax authorities, converting crypto values to fiat at the time of payment for accurate reporting.

AML and KYC compliance

Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements apply equally to crypto payroll providers as they do to traditional banks. Under the EU’s Markets in Crypto-Assets (MiCA) regulation and the evolving FinCEN guidelines in the US, platforms must verify the identity of every payer and payee. This means rigorous due diligence on contractor identities to prevent sanctions evasion. For global payouts, this adds a layer of administrative friction. Employers must confirm that their payroll platform maintains robust transaction monitoring to flag suspicious patterns, ensuring that the flow of digital assets does not violate international sanctions lists.

Contractor vs. employee classification

The most significant legal risk in crypto payroll is worker classification. Paying in crypto does not change the legal nature of the working relationship. If a worker is classified as an employee under local law, the employer must withhold income tax, social security, and unemployment contributions, regardless of the payment currency. Misclassifying an employee as an independent contractor to simplify crypto payments is a common pitfall that leads to heavy fines. The OECD’s guidelines on platform economy work emphasize substance over form; the level of control and integration determines status, not the asset used for compensation.

Stablecoin regulatory context

The choice of asset also impacts compliance. While Bitcoin and Ethereum are widely recognized as speculative assets, stablecoins like USDC are subject to specific reserve and transparency requirements under frameworks like the GENIUS Act in the US and MiCA in Europe. Employers must ensure that the stablecoins used for payroll are issued by regulated entities to avoid holding devalued or frozen assets. This regulatory clarity is essential for maintaining payroll continuity and trust among the workforce.

Top crypto payroll platforms compared

The crypto payroll market in 2026 is fragmented, with no single platform dominating every compliance jurisdiction. Employers must weigh supported chains, fee transparency, and legal coverage against their specific operational needs. While some platforms prioritize global reach, others focus on institutional-grade security or specific stablecoin integrations.

The following comparison highlights five leading platforms: Eco, Bitwage, Deel, Rise, and Toku. These providers represent the current spectrum of solutions, from early movers like Bitwage to newer entrants offering hybrid fiat-crypto structures.

| Platform | Supported Chains/Stablecoins | Fee Structure | Compliance Coverage |

|---|---|---|---|

| Eco | Multi-chain (ETH, SOL, Base, etc.), USDC/USDT | Variable by region; often subscription + transaction | Global contractor onboarding, tax reporting tools |

| Bitwage | Multi-chain, USDC, DAI | Per-employee monthly fee + transaction fees | 170+ countries, tax withholding support |

| Deel | USDC, USDT (via integrations) | Platform subscription + crypto payout fees | EOR services, local entity compliance, global payroll |

| Rise | Ethereum, Polygon, USDC | Transaction-based fees; no hidden platform costs | US-focused, 1099 contractor compliance |

| Toku | Multi-chain, USDC, DAI | Flat monthly fee + low transaction fees | Global, automated tax reporting, audit trails |

Implementation checklist for employers

Adopting crypto payroll requires a structured workflow that prioritizes regulatory compliance before technical deployment. Employers must treat this as a legal integration, not just a payments feature. The following steps outline the mandatory sequence for a secure rollout.

Before selecting a vendor, verify the legal status of wage payments in digital assets within your operating jurisdictions. Some regions classify crypto as property rather than currency, triggering capital gains tax events for employees. Consult local counsel to determine if stablecoins like USDC offer safer compliance pathways than volatile assets like Bitcoin.

Choose a provider that handles tax withholding, reporting, and fiat conversion automatically. The platform must integrate with your existing HRIS and accounting software. Ensure it supports "payroll-as-a-service" models where the employer pays fiat, and the platform distributes crypto, thereby avoiding direct custody risks for your company.

Establish clear internal policies regarding which employees are eligible, the percentage of salary payable in crypto, and the specific assets allowed. Create an employee handbook addendum that explains the risks, tax implications, and withdrawal procedures. This documentation is critical for mitigating liability if market volatility affects employee compensation.

Provide mandatory training on wallet security, private key management, and tax reporting. Employees must understand that crypto wages are taxable income at the time of receipt. Offer a hybrid option where employees can choose to receive partial payments in stablecoins to reduce volatility exposure while maintaining liquidity.

Launch with a small group of voluntary participants before full-scale adoption. Monitor transaction success rates, tax withholding accuracy, and employee feedback. Regularly audit the platform’s security certifications and ensure your internal accounting records accurately reflect the fair market value of crypto payments at the time of disbursement.

No comments yet. Be the first to share your thoughts!